What does 'AI bookkeeping' actually mean? (And what it doesn't.)

What is AI bookkeeping, and does it actually work? Search for the term in 2026 and you get a wall of vendor marketing. Here is the honest breakdown of what AI is genuinely good at inside the books, what it is not, and the two architecture choices that decide whether AI bookkeeping actually works or quietly fails.

Search for "AI bookkeeping" in 2026 and you get a wall of vendor marketing. Every accounting firm with a website has slapped the word "AI" on its services page in the last 18 months. Every software company has shipped a feature called "AI Assist." Almost none of them have explained what they actually mean.

This is the honest breakdown. What AI is genuinely good at inside the books, what it is not, what the marketing leaves out, and the two architecture choices that decide whether AI bookkeeping actually works in practice or quietly fails behind a clean dashboard.

If you are running a startup or a small business and you have been Googling "AI bookkeeping" trying to figure out whether this is real or hype, the answer is yes. Both. It is real, and most of it is also hype, and the trick is telling the difference.

What "AI bookkeeping" usually means in marketing

Start with what the term usually points at, because the marketing version is wide enough to mean almost anything. "AI bookkeeping" in vendor copy can refer to:

- A traditional bookkeeping firm that uses ChatGPT internally to draft client emails

- A QuickBooks add-on that auto-categorizes transactions using a rules engine vendors are calling "AI"

- An OCR tool that extracts numbers from receipt photos

- A managed accounting service where the bookkeepers happen to use AI tools alongside spreadsheets

- A true AI-native ledger where the books are kept by software with human accountants overseeing exceptions

These are not the same product. The first one is a firm with a productivity tool. The last one is a fundamentally different system. The middle three are software features in legacy products. If you are evaluating "AI bookkeeping" without naming which of these you actually want, the marketing wins.

The five functions inside bookkeeping (and where AI actually helps)

Bookkeeping is not one thing. It is at least five jobs that get bundled into one role. AI's usefulness varies sharply across them. The honest breakdown:

-

01

Transaction categorization

AI is genuinely good here. A model trained on your transaction history plus a few hundred businesses like yours can categorize 90% of new transactions correctly on the first pass. The remaining 10% are the ambiguous ones (was the deposit a refund or a new sale?) and those need a human. Marketing that says "AI categorizes your transactions" is true. The only question is whether the system surfaces the 10% for review or silently guesses.

-

02

Bank reconciliation

AI is partly good. Matching deposits to invoices and credits to payments is mostly pattern-matching, which models do well. But end-of-month reconciliation also requires investigating why the bank says $X and the books say $Y, which is detective work. A model can flag the discrepancy. Resolving it usually still needs a human who knows the business.

-

03

Anomaly detection

AI excels here. "This vendor charge is 4x the normal amount." "This invoice was paid twice." "This expense category jumped 60% month over month." Models notice these instantly. A human bookkeeper reviewing transactions line by line will miss the same patterns half the time. This is one of the cleanest wins for AI in finance.

-

04

Reporting and explanation

AI is good at presentation, not judgment. A model can write a clean monthly summary, draft a variance explanation, format a board-ready cash-flow chart. What it cannot do is decide whether a 15% margin compression matters strategically. That call still requires someone who knows your business and your goals. The best AI reporting tools surface the data and structure the narrative. The interpretation is yours.

-

05

Client and vendor communication

AI is hit or miss. Drafting a polite late-payment reminder? Fine. Negotiating a payment plan with a frustrated customer? Not yet. The work that looks routine (chasing AR, asking vendors for W-9s) actually requires relationship judgment in 20% of cases. Automating it without escalation paths produces awkward emails and burned relationships.

The role of humans (which the marketing always undersells)

Here is the part the vendor pages skip. Even with the best AI in finance today, you still need humans for at least four jobs:

Exception review. Every AI categorization decision needs an audit trail and a human who can override. Without that override, AI mistakes compound silently, and by month six your books have hundreds of small errors that nobody noticed because nobody was reviewing.

Judgment calls. Is this expense capitalizable? Should this revenue be recognized over 12 months or 24? Is this transaction related-party? These are not pattern-matching questions. They require an accountant.

Anomaly resolution. AI flags the unusual transaction. A human investigates why. Often the answer is innocent (one-time prepayment, vendor renegotiation), occasionally it is theft, sometimes it is a recording error from three months ago. The investigation is human work.

Strategic communication. Reporting facts is one thing. Explaining what they mean to a board, a lender, or an investor is another. AI can draft the email; a human decides whether the message is right.

A bookkeeping service that claims to be fully AI with no humans in the loop is selling you a system that will look great for six months and then quietly produce books you cannot trust.

That is the honest verdict. The good news is the inverse is also true: a system that pairs AI with the right human oversight is materially better than either AI-alone or humans-alone.

The two architecture choices that decide everything

Where AI bookkeeping actually breaks down, in our experience and in the public complaint record, is at the architecture level. Two choices matter most.

Architecture choice #1

AI on top of QuickBooks, or AI-native ledger?

Most "AI bookkeeping" services today are AI sitting on top of QuickBooks Online. Pilot is an AI service on QBO. Bench (rest in peace) was a custom UI on top of a fairly traditional ledger. Many newer entrants follow the same pattern because QBO is the default the customer is already on.

The problem: QBO was designed in the 1990s for accountants, not for software to read and write. Every "AI" feature has to translate intent into API calls QBO understands, work around fields QBO doesn't support, and reconcile discrepancies between what the AI thinks happened and what QBO actually recorded. The ceiling is the ledger.

AI-native ledgers (the newer model) own the system end to end. The agents read and write directly into the ledger. There is no translation layer. The data model can include things QBO can't, like reasoning traces, approval chains, and confidence scores on every categorization. The work happens in minutes instead of days.

Trade-off: AI-on-QBO lets you keep your existing accountant and your existing books. AI-native means migrating. Both are legitimate paths. Just know which one you are buying.

Architecture choice #2

Human-in-the-loop, or human-on-the-loop, or no humans at all?

The three patterns matter for very different reasons.

Human-in-the-loop: Every AI action goes through a human approval gate before it touches your books. Highest accuracy, slowest, most expensive. Right for high-stakes work like month-end close, tax filings, anything that touches the bank.

Human-on-the-loop: AI acts on its own confidence; humans review a sample or get pinged when something looks weird. Faster, cheaper, scales better. Right for high-volume routine work like daily transaction categorization.

No humans: AI runs unsupervised. Cheapest, fastest, and where you find the horror stories. Avoid for any system that touches financial records.

The right answer for a startup or small-business finance team is a mix: human-in-the-loop for close and money movement, human-on-the-loop for daily ops, never the third pattern. Ask any AI bookkeeping vendor which pattern they use for which function. If they cannot answer, they have not thought about it.

What to actually look for when you evaluate AI bookkeeping

If you are shopping for AI bookkeeping for your business right now, the questions that separate real products from marketing:

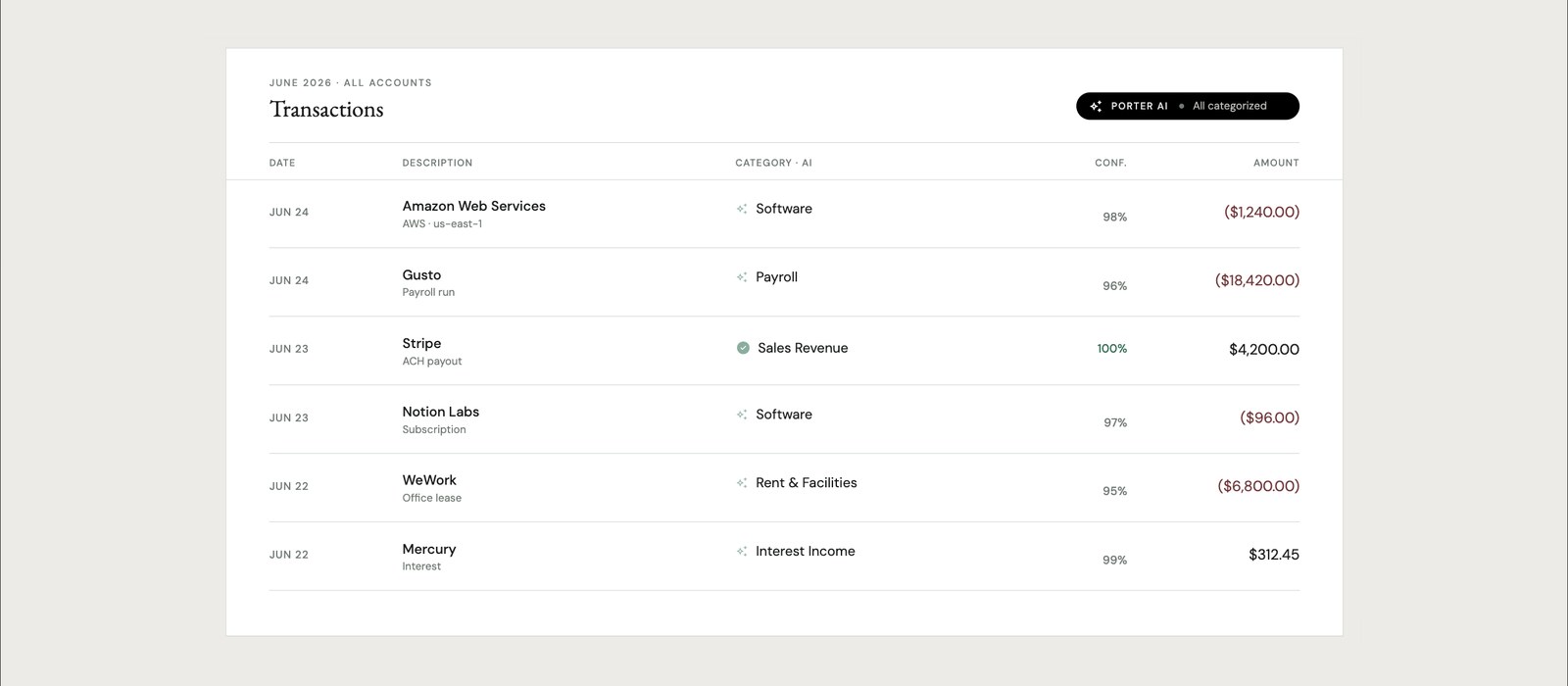

Does the AI explain its reasoning? When the system categorizes a transaction, can you click into it and see why? "We classified this as a marketing expense because the vendor's last 12 transactions were all categorized as marketing" is real reasoning. "Our AI suggests marketing" is not.

Where does the data live? If the AI is reasoning over QuickBooks, your data is in QuickBooks and you own it. If the AI runs on a proprietary ledger, ask how you get a complete export the day you leave. Bench customers learned this the hard way.

Who has the authority to move money? AI included. If the service can initiate payments without a human approval gate, that is not a bookkeeping product, that is a security liability. The median small-business fraud loss is $141,000 per incident according to the ACFE; you do not want to add automated payment authority to that risk profile.

How does the system handle the 10%? Categorization is 90% confident, 10% uncertain. What happens to the 10%? A real product has an exception queue with a human who reviews it within an SLA. Marketing pages that don't mention the 10% are selling you a system that silently guesses.

What changes when the AI is wrong? Errors are inevitable. The difference between products is what happens after. Does the system catch its own mistakes? Does it learn from corrections? Does a human review what looked unusual? If the answer is "we don't really track it," that is the answer.

The honest verdict

AI bookkeeping is real. Categorization, reconciliation matching, and anomaly detection are genuinely better with modern AI than with traditional firms that scaled by hiring more junior staff. The cost-to-quality ratio is also better, often substantially.

The hype is real too. Most products marketed as "AI bookkeeping" today are either traditional services using AI tools internally (fine, but not what the marketing implies), AI features bolted onto QuickBooks (capped by the underlying ledger), or autonomous systems with no human oversight (avoid).

The right architecture matters more than the AI model. A worse model in the right architecture (AI-native ledger, human-in-the-loop for high-stakes work, exception queues for low-confidence decisions) beats a better model in the wrong one. Ask the vendor about architecture before you ask about model.

A short word about us

Porter is an AI-native ledger that scales with the business and speaks the operator's language, not the accountant's. Categorization, reconciliation, AR follow-ups, AP capture, and anomaly detection run as AI agents inside the ledger. Human finance leads review every exception and approve anything that touches your bank accounts. Nothing posts without explicit human approval.

If you are evaluating AI bookkeeping for your startup or small business, we are happy to be one of the products you put through the questions above. Start here.

Sources cited:

- Association of Certified Fraud Examiners, small-business fraud statistics

- BBB and Capterra reviews of Bench Accounting, Pilot, and 1-800Accountant (2024 to 2025)

- TechCrunch coverage of Bench shutdown (December 2024)

- Porter customer interviews (March 2026), surfaced the "AI on QBO vs AI-native" architectural distinction

- Public Pilot, Kruze, and Xendoo product pages for the "AI bookkeeping" marketing patterns described

Common questions

01. What is AI bookkeeping?

A software category where AI models handle categorization, reconciliation, anomaly detection, and reporting inside the ledger, typically supervised by human accountants for exception handling and money-movement approval. It ranges from AI-on-QBO (features added to legacy tools) to AI-native ledgers built end-to-end for AI operation. The architecture matters more than the model.